What is the Cardiac Output Monitoring Devices Market Overview – definition, scope, and significance?

The Cardiac Output Monitoring Devices Market comprises technologies used to measure the volume of blood the heart pumps per minute, a critical indicator of cardiovascular performance. The scope includes invasive methods such as thermodilution and pulmonary artery catheters, as well as non‑invasive techniques like pulse contour analysis and bio‑impedance. These devices are essential in intensive care, surgery, and emergency settings, enabling clinicians to optimize fluid therapy, detect hemodynamic instability, and improve patient outcomes.

What are the main drivers, restraints, challenges, and opportunities in the Cardiac Output Monitoring Devices Market?

Key drivers include rising prevalence of cardiac disorders, expanding intensive‑care capacities, and growing adoption of minimally invasive monitoring in operating rooms. Restraints stem from high acquisition costs of advanced systems and the need for skilled personnel. Challenges involve stringent regulatory pathways and concerns over device‑related infections in invasive procedures. Opportunities arise from technological advances in wearable, non‑invasive sensors, and integration of data analytics for real‑time decision support.

What growth trends are currently shaping the Cardiac Output Monitoring Devices Market?

Current trends feature a shift toward non‑invasive and wireless monitoring solutions that reduce infection risk and improve patient comfort. There is increasing convergence of cardiac output devices with electronic health record platforms, facilitating seamless data flow. Moreover, emerging markets are investing in modern intensive‑care infrastructure, creating new demand pockets. The market also sees growing preference for single‑use consumables that enhance sterility and reduce turnaround time.

How has COVID‑19 impacted the Cardiac Output Monitoring Devices Market, and what is the recovery trajectory?

The pandemic accelerated demand for advanced hemodynamic monitoring as severe COVID‑19 cases often required precise cardiac output assessment. Supply‑chain disruptions temporarily slowed manufacturing, but heightened awareness of critical care needs spurred rapid adoption in hospitals. Post‑pandemic, the market is on a steady recovery path, with hospitals maintaining higher inventory levels and continued investment in monitoring capabilities to manage future respiratory and cardiac crises.

Who are the major competitors in the Cardiac Output Monitoring Devices Market, and what does the competitive landscape look like?

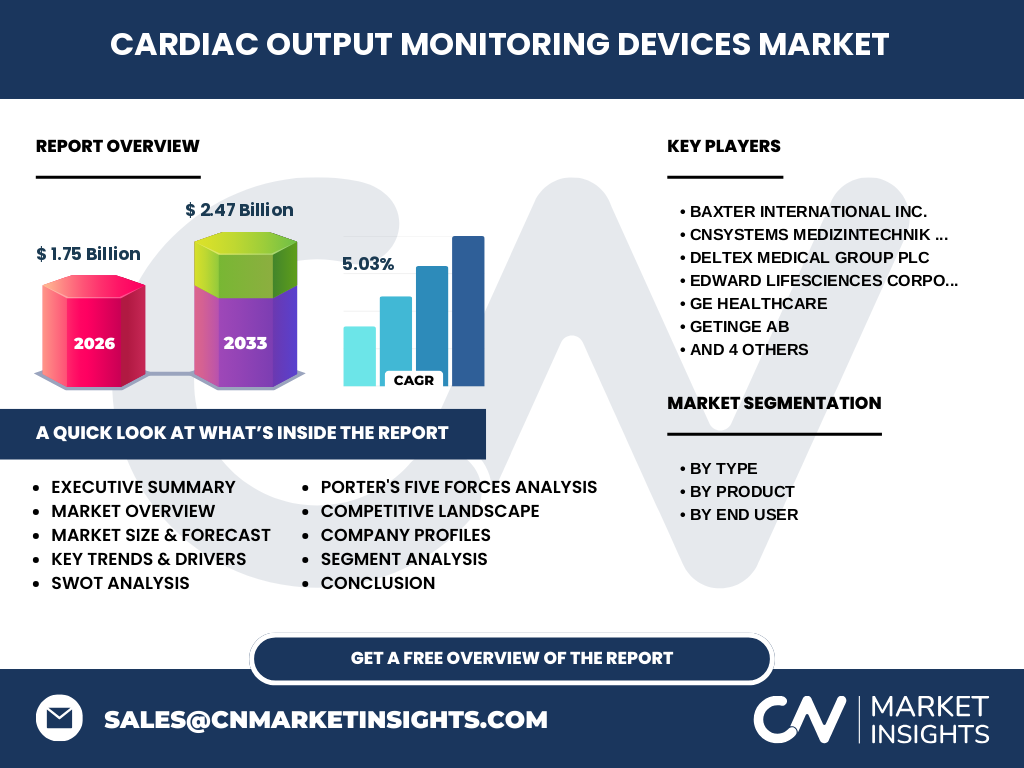

The market is moderately consolidated, led by global players such as GE Healthcare, Baxter International Inc., and Edwards Lifesciences Corporation. Other notable competitors include CNSystems Medizintechnik GmbH, Deltex Medical Group plc, Getinge AB, ICU Medical Inc., LiDCO Group plc, Osypka Medical GmbH, and Uscom. Companies compete on technology innovation, product portfolio breadth, and strategic partnerships, while occasional mergers and acquisitions aim to strengthen market position and broaden geographic reach.

What are the key findings in the executive summary of the Cardiac Output Monitoring Devices Market?

The market reached a valuation of US 1.75 billion in 2026 and is projected to climb to US 2.47 billion by 2033, reflecting a compound annual growth rate of 5.03 %. Growth is driven by increasing cardiovascular disease burden, expanding critical‑care capacity, and a clear shift toward non‑invasive monitoring. Competitive dynamics revolve around innovation and strategic collaborations, while regional demand is strongest in North America and Europe, with emerging growth in Asia‑Pacific.

What are the forecast expectations for the Cardiac Output Monitoring Devices Market from 2025 to 2032?

Based on the provided CAGR of 5.03 %, the market is expected to continue expanding steadily through 2032. The forecasted size of US 2.47 billion for 2033 suggests incremental growth each year, supported by ongoing adoption of advanced monitoring technologies, rising healthcare expenditures on critical‑care equipment, and increasing focus on patient safety and outcome optimization.

How is the Cardiac Output Monitoring Devices Market sized and shared by segmentation?

Segmentation by type divides the market into invasive and non‑invasive devices, each serving distinct clinical scenarios. By product, the market separates into consumables, accessories, and instruments, reflecting the recurring revenue from disposables and the capital spend on hardware. End‑user segmentation includes hospitals and ambulatory surgical centres, with hospitals accounting for the larger share due to intensive‑care demands, while ambulatory centres drive growth for portable, non‑invasive solutions.

What is the global market size and share of the Cardiac Output Monitoring Devices Market by region?

The global market stands at US 1.75 billion in 2026. While specific regional revenue figures are not disclosed, the market is broadly distributed across North America, Europe, Asia‑Pacific, and the Rest of the World. North America and Europe together hold a dominant share owing to mature healthcare systems, whereas Asia‑Pacific exhibits faster growth potential driven by expanding hospital networks and rising awareness of advanced cardiac care.

What does the regional analysis reveal about the Cardiac Output Monitoring Devices Market?

In North America, high adoption rates are linked to advanced ICU infrastructure and strong reimbursement frameworks. Europe benefits from well‑established clinical guidelines that promote continuous hemodynamic monitoring. Asia‑Pacific shows the most rapid expansion, propelled by increasing investments in modern hospitals and a growing middle‑class population seeking high‑quality cardiac care. Emerging markets in Latin America and the Middle East are also beginning to allocate resources toward critical‑care monitoring.

What are the profiles and strategies of leading companies in the Cardiac Output Monitoring Devices Market?

GE Healthcare focuses on integrated diagnostic platforms combining cardiac output monitoring with imaging. Baxter International leverages its broad product portfolio to cross‑sell consumables and accessories. Edwards Lifesciences prioritizes innovative minimally invasive technologies. CNSystems specializes in non‑invasive bio‑impedance solutions. Deltex Medical emphasizes portable, easy‑to‑use devices for surgical suites. Getinge and ICU Medical expand through strategic acquisitions, while LiDCO, Osypka, and Uscom concentrate on niche markets and customized solutions.

How does Porter’s Five Forces analysis apply to the Cardiac Output Monitoring Devices Market?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of suppliers is relatively low as most components are commoditized, but specialized sensor manufacturers retain some leverage. Buyers—primarily hospitals—exercise strong negotiating power through bulk purchasing and tenders. The threat of substitutes is limited because accurate cardiac output measurement remains essential, though non‑invasive technologies are gradually reducing reliance on invasive catheters. Rivalry among existing firms is intense, driven by rapid innovation cycles and the pursuit of market share.

What are the SWOT insights for the Cardiac Output Monitoring Devices Market?

Strengths: Critical clinical relevance, steady demand from intensive‑care units, and robust technology pipelines.

Weaknesses: High device cost and dependence on skilled operators.

Opportunities: Expansion of non‑invasive and wireless solutions, integration with AI‑driven analytics, and growth in emerging economies.

Threats: Regulatory scrutiny, potential market saturation in mature regions, and competition from alternative hemodynamic assessment tools.

What does the value chain of the Cardiac Output Monitoring Devices Market look like?

The value chain begins with research and development, where firms design sensors and algorithms. Component sourcing follows, often involving specialized electronics and medical‑grade plastics. Manufacturing encompasses assembly of instruments and production of single‑use consumables. Distribution channels include direct sales to hospitals, distributors, and online platforms for accessories. After‑sales services such as calibration, training, and maintenance complete the chain, ensuring device reliability and customer retention.

What key investment insights can be drawn for the Cardiac Output Monitoring Devices Market?

Investors should focus on companies that demonstrate a balanced portfolio of invasive and emerging non‑invasive technologies, as this mitigates risk while capturing growth. Strategic partnerships with clinical research institutions can accelerate product validation. Companies that enhance digital connectivity and data analytics capabilities are positioned for higher margins. Additionally, targeting emerging markets through localized production or joint ventures can unlock untapped demand.

What concluding observations summarize the Cardiac Output Monitoring Devices Market?

The market is on a solid upward trajectory, underpinned by a 5.03 % CAGR and expanding clinical need for precise hemodynamic data. Technological innovation, especially in non‑invasive monitoring, is reshaping product offerings and broadening end‑user adoption. While cost and regulatory factors present hurdles, opportunities in emerging regions and digital integration provide compelling growth pathways for manufacturers and investors alike.

How was the research for this report conducted?

The methodology combined primary interviews with key opinion leaders, hospital procurement officers, and device manufacturers, alongside secondary analysis of published industry reports, regulatory filings, and financial statements of major players. Market sizing employed a top‑down approach using known global healthcare expenditure trends, adjusted by the provided market size and forecast figures. Trend analysis was derived from technology adoption studies and pandemic impact assessments.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by type, product, and end‑user, as well as regional performance, competitive dynamics, and forward‑looking forecasts up to 2033. Limitations include reliance on publicly available data and the absence of proprietary sales figures for individual companies, which constrains precise market‑share quantification. Nonetheless, the analysis provides a comprehensive qualitative and quantitative overview useful for strategic decision‑making.

Which key companies are active in the Cardiac Output Monitoring Devices Market and what recent developments have they announced?

Among the leading firms, GE Healthcare launched a next‑generation wireless cardiac output monitor with integrated AI analytics. Baxter International introduced a new line of disposable thermodilution kits aimed at reducing procedure time. Edwards Lifesciences announced a partnership with a major university to develop minimally invasive sensor technology. CNSystems released an updated bio‑impedance platform for outpatient monitoring. Deltex Medical unveiled a compact, battery‑operated device designed for ambulatory surgical centres. Getinge and ICU Medical both reported recent acquisitions of niche accessory manufacturers to broaden their product ecosystems.